Establishing Shot

Establishing Shot

What is financialization?

Introduction

This piece is a kind of establishing shot. In a film, the establishing shot provides an overview of the setting and provides markers as to timeframe. Here we do the same by looking at financialization and providing an overview of current uses. The following focuses primarily on academic literature because the genre includes literature reviews, a standard form of meta-scholarship in which a researcher maps patterns of usage.

This exercise provides a common starting point, a building block. As we will see, a survey of financialization does not provide a foundation simply because the term designates socially and historically contingent and particular parallels and inter-relationships; it is not an object in the world, the features of which are given along with it, on the order of a table or a rock. But we can nevertheless use the term with clarity by attending to “family resemblances.”

After a brief discussion of some recent work that operates in that way, we lean on recent literature reviews to outline three basic levels of usage, gravitational centers if you like, that can be seen in recent work.

Aside: How We Plan to Proceed. Recognitions is in part a writing experiment through which we hope to achieve a balance between laying out the basics of finance and financialization and reporting on the impacts in particular schools across the country and, crucially, on how people are organizing around them to protest or mitigate or reverse them. We’ll do this in part by generating different series of texts. “Demystifying Finance” is one of those series. One way we’ve decided to work toward that balance (and control for length) is to make separate explainer documents--The Basics--that you can link to from the main text if you like. For example, the piece below links out to an explainer “What is the finance sector?” We’ll try to be consistent about providing these documents. We’ll provide a glossary of financial instruments that lists them by type, explains their basic characteristics, how they trade (if they do) and so on. We’ll also link out on certain elements of finance jargon to explanatory material available on the net.

Finance seems opaque because it comes couched in a slang that communicates with precision to insiders while excluding outsiders. Part of the demystification process is getting used to the slang, getting hip to the jive.

As one would expect, most links will take you to the material that’s being cited or to related articles that may be of interest—which is which should be clear from context. There will ringers from time to time, when we can work them in, pop songs for example.

What is Financialization?

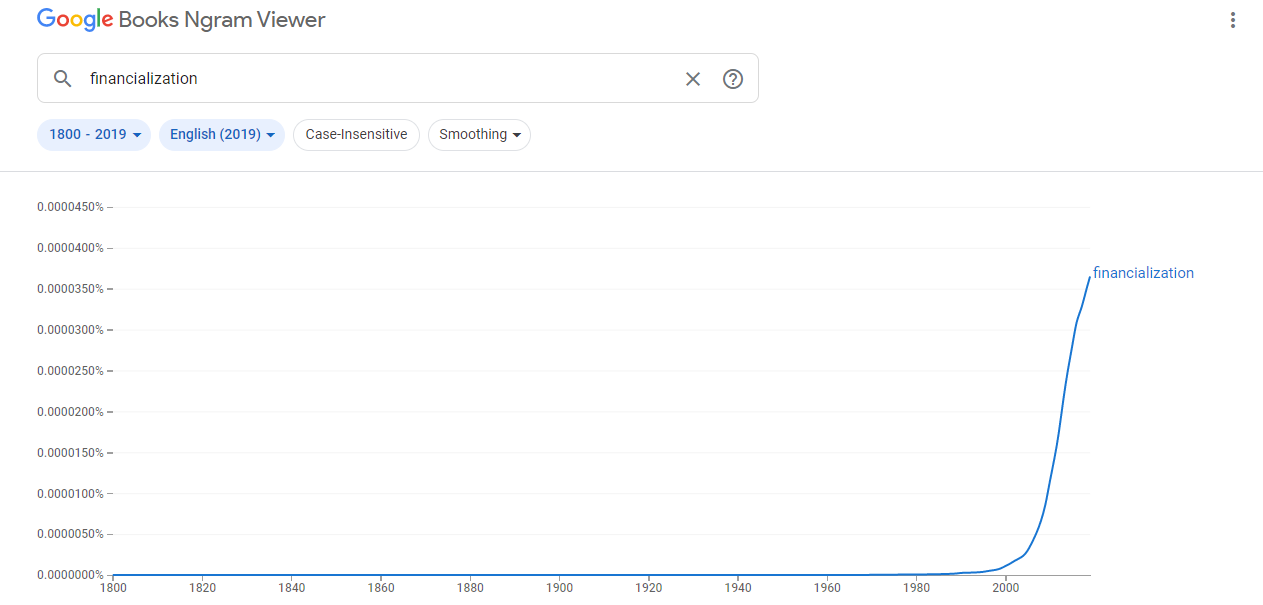

A Google™ N-gram shows that, for nearly 200 years, no-one talked about financialization. Then, in the late 1990s, people started to talk about it; soon, many people were talking about it.

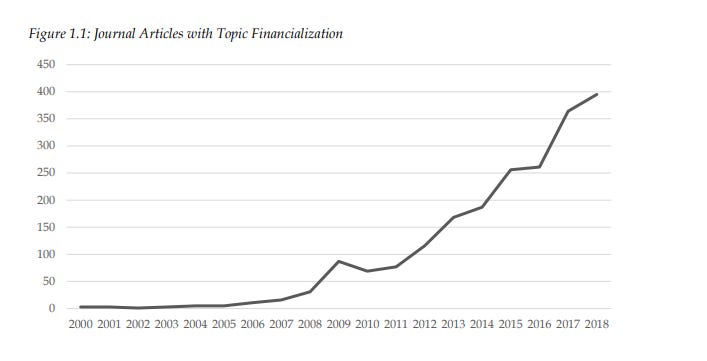

As they have for the past decade, Routledge tries to publish a guidebook when their acquisitions editors determine an academic fashion or approach has arrived. In their introduction to one such, The Routledge International Handbook of Financialization, authors and co-editors Philip Mader, Samuel Maartens and Natalie van der Zwann include some other frequency-of-use graphics:

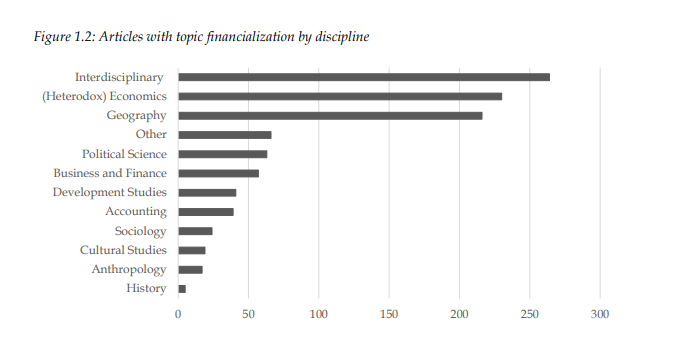

Keyword frequency is a useful proxy for interest; the next graphic shows that this interest is cross- disciplinary:

From the above we learn that lots of people are talking about financialization and that they do so from a range of perspectives. But what is it?

In 2008, Ronald Dore wrote:

Financialization is a bit like globalization, a convenient word for a bundle of more or less discrete structural changes in the economies of the industrialized world.

The Routledge Handbook opens with a more colorfully elaborate version of the same basic point:

In countries across Asia, variations on a parable are told. A group of blind men encounter an elephant and, having never “seen” one before, one boldly reaches out, feels the elephant’s leg, and tells the others that it is very much like a tree. A second touches its side, and reports that the elephant is, in fact, quite like a wall; a third touches the trunk and finds it is a big snake; another touches the tail (a rope); another its tusk (a spear); and so on. Depending on the variant, the parable ends either with the blind men disagreeing about the nature of the beast, perhaps even coming to blows over it, or with them wisely conferring on what they have learned, understanding that each was only partially correct, and recognizing that only together could they fully comprehend the beast.(2)

But, the authors hasten to add, while the parable might capture the state of financialization as an analytic category, the story should not be taken to imply that those who use it are blind. Rather, it follows that:

…very different approaches having led to divergent claims about the nature of financialization. This has involved tendencies to regard financialization as primarily, or essentially, one particular thing: as the increasing power of financial interests over politics, as the growing dominance of financial logics or ‘shareholder value’, as changes in the spatial organization of the global economy, as the reconfiguration of society and the class system, or as the mutation of culture and how we relate to ourselves. Yet these are not mutually exclusive, and only together give the whole picture.

Seemingly for chronological reasons, many attempts at specifying financialization take as a point of departure Gerald Epstein’s 2005 definition:

Financialization refers to the increasing importance of financial markets, financial motives, financial institutions, and financial elites in the operation of the economy and its governing institutions, both at the national and international levels.

Epstein also wrote in the same introduction to the 2005 collection Financialization and the World Economy:

Some scholars have insisted on a much narrower use of the term: the ascendancy of shareholder value as a mode of corporate governance, or the growing dominance of capital-market financial systems over bank-based financial systems.

As we will see, current patterns of usage can be roughly grouped and this grouping combines the registers Epstein distinguishes. But these patterns emerge through a heavy volume of uses, and some literature reviews (a standard form of academic writing) give voice to concerns that this volume in itself threatens to drain “financialization” of meaning. Mader, Maartens and van der Zwann fret that the term may come to stand for everything and signify nothing. To counter this, they suggest that analysts draw limits around the term, attending to specific mechanisms and social locations while also remaining alive to context (not least to the peculiarities of US capitalism) (p. 10). “Financialization,” they argue, should be understood as a process (or a cluster of processes) among others.

These writers make an argument is parallel to that developed by J.K. Gibson-Graham with reference to “capitalism”: that, in the current environment, it is as important, analytically and politically, to stipulate what capitalism is not as to stipulate what it is. In The End of Capitalism (As We Knew It): A Feminist Critique of Political Economy, they show that the conflation of all profit-seeking activity across all space and time with “capitalism” (as one frequently hears done) is a political and epistemological mistake that forecloses the space required to think about/imagine alternatives. They follow Marx in arguing that capitalism can be defined by the organization of production (the technology-centered decomposition of operations, standardization of tasks, deskilling of work) and wage relations (which Marx saw as predicated on the organization of production). Most types of service provision are not capitalist (though some, like Amazon, are.) Nor is artisanal work. Nor, for that matter, is trade. Delimiting capitalism means that we don’t have to project alternatives to capitalism into a future in a manner like science fiction—we just need to look at what is around us and consider possibilities or potentials that might be extrapolated into alternatives.

Maartens et al attribute the multiplicity designated by the term ”financialization” to the volume and range of disciplinary perspectives brought to bear on it. But it also reflects characteristics of what the term is used to designate. “Financialization” does not designate an object like a table or a rock, something the defining features of which are given along with the object itself. It may not then be best understood as a name or a category, but rather as a term that designates or points toward phenomena, processes or states of affairs that are held together by “family resemblances.”

In Philosophical Investigations, Ludwig Wittgenstein takes usage in ordinary language as a point of departure and shows that words are not always used to designate sharply delineated semantic spaces. He points to the notion of games which, he argues, groups together a range of activities, not because they share an set of essential defining features or predicates (as would tables or rocks), but because they share“a complicated network of similarities, crisscrossing and overlapping, sometimes overall similarities, sometimes similarities of detail” (para. 66). He continues:

I can think of no better expression to characterize these similarities than “family resemblances”; for the various resemblances between members of a family, build, features, color of the eyes, gait temperament etc. overlap and crisscross in the same way. And I shall say: ‘games’ form a family. (67)

In the course of the development that follows Wittgenstein does not exclude that words be imagined on the model of a category—indeed there are usages that rely on it. Rather, he suggests that there are also usages that neither admit of it or require it. “Games” designates a multiplicity of resemblances and attending to such multiplicities is a way of knowing. Look, he says, don’t think (categorically).

Aside 1 An explanation for why words are understood, quasi-automatically, in the manner Wittgenstein pushes could generatively begin with Marshall McLuhan’s 1962 book The Gutenberg Galaxy: The Making of Typographic Man.

“Financialization” may not simply be blurry due to overuse for two reasons. First, like “games,” it designates a multiplicity of processes and phenomena that can be grouped together because, at one level or other, they resemble each other. These resemblances can arise from any number of directions, from direct influences to having developed at the same time, in the same overarching contexts, the same air. At the same time, it can be treated categorically, in terms of a discrete meaning, with a clarity of boundaries that separate inside from out, and that can function tactically, to delimit and distinguish in the manner suggested by Gibson-Graham. Second, financialization points to processes and phenomena that are still social-historically emergent--whence the importance of looking at what is in front of you, so to speak.

There are recent publications that explore other avenues toward similar ends. Of these, I want to draw your attention to Grégoire Chamayou’s recently translated The Ungovernable Society: A Genealogy of Authoritarian Liberalism (should be libertarianism[1]) and to recommend it as it informs our recent thinking. The book tracks aspects of what, retrospectively, we might call the pre-history of financialization in libertarian/conservative responses from American “business” to the social and political upheavals the late 1960s-early 1970s. These business people occupied a considerable diversity of subject positions. Chamayou writes:

For my investigation, I have gathered various heterogenous sources from different disciplines; I decided to intertwine “noble” and the “vulgar” sources where they have the same object-thus a Nobel Prize winning economist may rub shoulders with a specialist in union-busting. Their writings are all strategic texts in a struggle, and they all answer the question “What is to be done?”

The struggle that Chamayou refers to is a family resemblance, and the strategies they devised another. When these businessmen looked out from where they were at the civil rights movement and the opposition to Vietnam, at the mounting criticisms of capitalism and questioning of hierarchies, they saw “a crisis of governability.” They saw democracy run rampant. Many blamed university Humanities departments for disseminating “cultural Marxism.” This loose-knit business community sought, from different starting-points and by different means, to curtail this democracy and re-establish order based on what they saw, in libertarian terms, as a natural hierarchy. Chamayou provides a strong sense of the various projects devised to push back at the excesses of the wrong types of freedom while also providing, by the way he proceeds as a writer, a portrait of a group that emerges clearly only in retrospect, through the effects of their actions, effects that have been revealed by “neoliberalism’s” legitimation crisis, ongoing since at least 2008, compounded and deepened by the variously botched responses to the COVID-19 pandemic. Chamayou manages this portrait by creating a prose collage. He describes his approach at the end of his introduction:

I often keep myself in the background in this book so as to reconstitute, by cutting and editing quotations, a composite text whose assembled fragments whose assembled fragments are often worth less individually (…) than as utterances characteristic of the different positions to which I have tried to give voice. (6)

You can see parallels to Chamayou’s approach to his single work in some calls to re-orient the work of many researchers around shared overall perspectives that leave space for the emergent characteristics of an increasingly financialized reality. Eve Chiapallo (who co-wrote with The New Spirit of Capitalism with Luc Boltanksi and whose subsequent work on valuation is very interesting) has been calling for the latter kind of work. The sensibility is shared by people writing from STS, sociology of finance and accounting, the anthropology of finance and others. Writers from these spaces often refer to “micro-technologies” that can be material, socio-political or more broadly metaphorical where a reader of Wittgenstein might talk about family resemblances.

Earlier, I mentioned that recent literature reviews group the main uses of “financialization,” and that these groupings combine what Epstein considered more and less narrow implications. Natascha van der Zwaan’s 2014 “State of the Art: Making Sense of Financialization” is pretty representative of these reviews. Van der Zwaan’s extensive review shows that contemporary usages of financialization can be sorted into three basic levels. Financialization is used:

· to designate a regime of accumulation (across the 1970s, factories gave way to finance in short)

· to discuss the transformations of corporate governance brought about, directly or indirectly, by the cult of shareholder value

· to refer to the colonization of everyday life by finance, financial instruments and ways of talking or thinking derived from or influenced by finance.

Let’s look at each in turn:

Regime of accumulation is a term developed by the French Regulation School of economics. Many analysts who talk about financialization in these terms refer to Greta Krippner’s definition, taken from her 2011 Capitalizing on Crisis:

Financialization is a "pattern of accumulation in which profit making occurs increasingly through financial channels rather than through trade and commodity production.

The definition points to the dominant socio-economic arrangement in the US, and to the increased importance of “financial channels.” It makes intuitive sense that financial channels be defined as “not trade” and “not commodity production” but provides no real footing to say what financial channels are. One could say: “The sum of these financial channels is the finance sector.” But that would not get one far toward a sense of what the finance sector is materially. We venture a partial discussion in “The Basics: What is the Finance Sector” that can be found here [hotlink].

One might be inclined to quantify Krippner’s expression “growing importance,” but precision is greatly hampered by the fact that there is no agreed-upon definition of the finance sector as a datapoint. A recent McKinsey report discusses this problem (to read the report is to take a plunge into contemporary management-speak). With that imprecision in mind, the relative importance of finance varies with whether it is measured, as it typically is, in terms of revenues, market capitalization or assets under management.

· In 2018, finance and insurance revenues (as a sector) summed to $1.5 trillion, which represented 7.4 percent of that year’s U.S. GDP..

· At the close of trading on September 29, 2020, the publicly-traded financial sector had a combined market capitalization of $5.59 trillion which represented 10.5% of the stock market’s end-of-year total of $53 trillion.

· Measuring the scale of the financial sector by adding assets under management provides numbers in excess of total GDP that might also be seen as indicators of the extent to which finance dominates imaginations. Relations of AUM to GDP are clearest, and most fun. when represented graphically. The St. Louis Federal Reserve’s FRED database provides one such graphic here. The World Bank compiles statistics on the value of traded stocks as a percentage of GDP. A more complete picture would take debt instruments into account. The Bank of International Settlements compiles data on trade volumes in debt securities (and derivatives) that can be accessed through this main page.

Krippner’s definition leaves implicit what many critics take as central: that the rise of the financial sector has come at the expense of others forms of economic activity. Rising inequality has been another social price exacted by the rise of finance. Both are exceptionally important; we will take them up in the future of this project.

It is less the relative position of finance per se that’s been so damaging than it is the hold it exerts on imaginations both for what it frames in and what it frames out, what it enables and what it dissolves. The next section talks about recent, dysfunctional changes to corporate governance by way agency theory.

Transformation of management under the sign of shareholder value Van der Zwaan’s second level isolates financialization as it refers to transformations of corporation governance, or how corporations are run, under the influence of the doctrine of shareholder sovereignty. The doctrine originated with neoliberalism and is associated with Milton Freidman, but it was made operational via Michael Jensen’s agency theory, which was particularly influential as figured in the reorientation of business schools (and rise of finance economics) across the 1970s. This reorientation moved away from management and toward finance; it was particularly evident at the MBA level and redefined “administration.”

The idea of s shareholder sovereignty come out the libertarian (neoliberal) right, notably the economists who comprised the Mount Pelerin Society. The history Mount Pelerin, and of neoliberalism proper (that is of the relatively small group who understood themselves as “neoliberal”) has been extensively documented: Quinn Slobodian’s Globalist: The Rise of Neoliberalism and the End of Empire is a recent, good addition to that literature. Neoliberalism is also associated with the Economics Department at the University of Chicago, the long-time institutional home of Milton Friedman among others. Freidman is known as an advocate for the position that corporations have an ethical imperative to maximize shareholder returns to the exclusion of everything else. This simplified version of his position was published as a 1970 article in the New York Sunday Times, one that has since had an outsized impact.

Neoliberal discourse drew heavily from the work of Frederich von Hayek on the nature and virtues of “free markets” and “deregulation”. (a sympathetic presentation of his bio and ideas is here.) They made a fetish of the private (as over the always incompetent and slow governments and the public interest it represents). They managed for a time to substitute the figure of the heroic entrepreneur (as over against the fossilized bureaucrat) for the firm as the basic unit for thinking economic activity. Neoliberal discourse generally opposed the pubic and to accountability to the public. Their libertarian rhetoric carried for a while a sense that freedom of markets was symmetrical with freedom in political terms, but it was clear to many observers from early on that this sense was false. They pointed to the relationship between the Chicago Boys and Pinochet’s dictatorship in Chile after 1972 and the ease with which “free markets” and authoritarian politics coexisted. The history is instructive; a point of departure can be found here.

Shareholder value is informed by a libertarian definition of property ownership as control, made over into a theory of corporate governance in the mid-1970s by Michael Jensen and named “agency theory.” An outline can be found here and here. Grégoire Chamayou’s book, mentioned earlier, includes is very useful for understanding agency theory and Jensen’s very rightwing political commitments.[2] Agency theory is fundamental for finance economics, where it is introduced in graphic form as a map of The Firm adequate to reality in every introductory course. The influence of agency theory is pervasive in finance regulation, particularly in auditing rules.

It is also hugely problematic. Chamayou’s foregrounds the degree to which agency theory was based on a book a libertarian rejection of the description of the modern corporation at the heart of Berle & Means’ 1932 book The Modern Corporation and Private Property, a summary of which can be found here. The problem, from that viewpoint, was Berle & Means’s view of manufacturing (their paradigmatic type of Firm) which in its organization introduced, de facto, a separation between ownership (shareholders) from control (management). Taken de jure, they argued, this separation cut to the quick the common-law definition of property ownership.

Space does not permit much development, but suffice it to say that Berle & Means develop a map of The Firm that included spaces of manufacturing in which workers and unions vied with management for control over the process. Executive levels worked to outline set targets, manage cash flows, etc. (This returns below via Mike Konczal). Efficiencies—always a battleground on the shop floor—were defined relative to production targets.

Jensen rejected the idea that ownership can be separated from control. To effect this, he re-centered the map of The Firm. The new map envisioned shareholders as activist owners (as opposed to passive stewards, as they had been imagined previously) and their interest (returns) as paramount. CEOs and CFOs are at the map’s center; the agent problem (that they might act in their own interests) is resolved though “incentive alignment” that is by pegging compensation to share price via “performance-based” bonuses. Agency theory relocates efficiency from the space of production, where it was based on production speed, to that of accounting, where it is based on stock share price framed as an indicator of a company’s performance. A firm operates efficiently when it maximizes its share price and, by extension, shareholder returns. At the outer edge of the meaningful world, one finds management, which agency theory frames in adversarial terms, as perpetually acting in its own self-interest. The recentering came at the expense of spaces of production; it eliminated workers and, especially, unions; any space for workplace democracy was erased, along with any sense of responsibility to stakeholders, apart from shareholders (agency theory’s only stakeholders, who acquire the status via ownership)

This truncated map of the firm came wrapped in Freidman’s claim that maximizing shareholder returns is an ethical imperative. Self-enrichment is therefore good; inequality a natural by-product and so on. The same rhetoric of ethics allowed the virtual erasure of the non-financial consequences of financial actions (this is characteristic of contemporary financialized capitalism more generally). The consequences people acting on the world with motives and understanding shaped by this worldview have been enormous, even as, on a descriptive level, agency theory admits of a broad range of possible uses/roles (the correlation/causation problem). Agency theory is a diagram of narcissism.

The impact of agency theory has been significant at the level of managerial practice. Mike Konczal provided a good synopsis in his 2014 article for Washington Monthly, “Frenzied Financialization,”

…Financialization isn’t just confined to the financial sector itself. It’s also ultimately about who controls, guides, and benefits from our economy as a whole. (…) The “shareholder revolution,” started in the 1980s and continuing to this very day, has fundamentally transformed the way our economy functions in favor of wealth owners.

To understand this change, compare two eras at General Electric. This is how business professor Gerald Davis describes the perspective of Owen Young, who was CEO of GE almost straight through from 1922 to 1945: “[S]tockholders are confined to a maximum return equivalent to a risk premium. The remaining profit stays in the enterprise, is paid out in higher wages, or is passed on to the customer.” Davis contrasts that ethos with that of Jack Welch, CEO from 1981 to 2001; Welch, Davis says, believed in “the shareholder as king—the residual claimant, entitled to the [whole] pot of earnings.”

This change had dramatic consequences. Economist J. W. Mason found that, before the 1980s, firms tended to borrow funds in order to fuel investment. Since 1980, that link has been broken. Now when firms borrow, they tend to use the money to fund dividends or buy back stocks. Indeed, even during the height of the housing boom, Mason notes, “corporations were paying out more than 100 percent of their cash flow to shareholders.”

Management as a category finds itself in a paradoxical situation under sign of shareholder sovereignty. (Outlines of the broader story of contemporary management ideology can be found here for example.) On the one hand, agency theory casts it to the outer edge of the meaningful world. On the other, management has been subjected to an intensive automation under the aegis of various schools, the most famous of which is New Public Management. NPM is particularly important as a point of departure for understanding academic administrations and their transformations as it translates the world according to agency theory to an administrative context not owned by shareholders or governed by the same imperatives. NPM enjoins public-sector administrators to import private-sector, for-profit attitudes and processes into non-profit spaces using a pervasively libertarian rhetoric about government, bureaucracy on the one hand, spunky entrepreneurialism and innovation on the other. In higher education, versions of NPM were associated with the implementation of metrics, notably bibliometrics. The impact of NPM on faculties is the topic Chris Lorentz’s 2012 essay in Critical Inquiry, “If You're So Smart, Why Are You under Surveillance? Universities, Neoliberalism, and New Public Management.” Lorentz’s essay is an early (and highly polemical) attempt at naming (the problem he takes on is stated in the essay’s epigraph, a quote from sociologist Pierre Bourdieu).

Lorenz’s piece defaults almost immediately into framing university “administration” simultaneously as an abstraction and as the Enemy, which can be satisfying in an exercise of naming, but which comes at the expense of a more complex and comprehensive picture of administration that may be able to point beyond financialization.

Agency theory can be understood as a cognitive map shared by people who have passed through MBA programs, where it plays a foundational role in defining the world according to Finance 101 world into which MBA students are entering. It is a colonization of the imagination for which b-school functions as a mechanism. The third register in van der Zwaan’s typology speaks to a broader imaginative colonialism.

The colonization of everyday life by finance, financial instruments and ways of talking or thinking derived from or influenced by finance.

Work on this register is said to explore ground opened by Randy Martin. For our purposes is not Martin per se, but a quote he pulled from Michael Mandel’s 1996 The High-Risk Society: Peril and Promise in the New Economy and included in his 2002 The Financialization of Everyday Life:

Historically, activities on the financial markets – the buying and selling of stocks, bonds, and other financial instruments – have been regarded as far different from the day-to-day endeavors in the real world. . . This distinction is quickly disappearing, as the high-risk society becomes as fluid and as competitive as the financial markets. . . The combination of high uncertainty and unrestricted competition is reducing the difference between the real economy of factories and offices on the one hand, and the financial markets on the other. The rules governing Wall Street now apply to the entire economy.

The implication: In the high-risk society, workers, businesses, and countries must start thinking like investors in the financial markets, where the only way to consistently achieve success is to accept risk. (p. 34)

While Mandel’s first paragraph works best when “rules” are understood metaphorically, the main point of the passage is clear enough: the main consequence of financialization for many people is a more precarious life. In many sectors, notions of career or job security have been erased as an effect of a conceptual shift in the status of labor from fixed to variable cost. This shift is central to the logic of outsourcing and off-shoring, which have long been central to the management-consultant business model of firms like McKinsey and Boston Consulting. A few moments reflection will show how agency theory contributes to this; a few more will show that, among innovations of financialized capitalism is new ways to produce the outcomes described by Marx in 1860 at the level of relations of production, to render people abstract and interchangeable “bearers of quanta of labor power.” Interchangeable people are disposable people. Consider the situations of adjuncts in contemporary higher education. Herb Childress’ The Adjunct Underclass: How America’s Colleges Betrayed Their Faculties, Their Students and Their Mission provides a clear and useful overview of the phenomenon. A interview with Childress from Inside Higher Ed is here, a review here.

The impact of financializaton on education in the US is not limited to colleges and universities. Jack Schneider and Jennifer Berkshire’s A Wolf at the Schoolhouse Door: The Dismantling of Public Education and the Future of School is an important overview of the current state of politically-motivated austerity play around K-12 systems nationally that focuses particular attention on the Right’s ongoing project of wrecking public education (and eliminating union teachers). A recent article from Stephanie Farmer shows with clarity the impact of financialization of the Chicago Public School System.

Another way of looking at precariousness is to see it as forcing people to take on risk management in the context of being an entrepreneur of one’s own life. One dimension of this was discussed in Boltanski and Chiapallo’s 2000 book The New Spirit of Capitalism., The dissolving of traditional career trajectories, they argue, and the accompanying sense of an exacerbated and intimate danger/risk was giving rise to a new sociological type: Network Man. Where a traditional career path once was there is networking, making connections, using others (instrumentally) to facilitate the movement from job to job. Where a traditional career trajectory might have had one looking forward, Network Man is always looking horizontally. Examples of Network Man (or Woman) can be found among college presidents and upper administrators who migrate place to place, job to job, forming what might be visualized as a lattice of the same people doing the same jobs in different spaces that, increasingly, look the same.

Our imaginations have been colonized by the language of finance as well. The mechanisms are ubiquitous. Consider for example that, prior to 1972. the major television networks’ nightly news programs used GDP indicators as their nightly barometer of the common weal: after GDP indicators were replaced with the Dow Jones Industrial Average. Night in, night out viewers are enjoined to identify their well-being with that of capital. It is not hard to extrapolate from there.

As Randy Martin rather dramatically put it:

…a colonizing of the daily life of middle-class Americans in ways analogous to how globalization is colonizing South American coffee growers or African cocoa farmers – by turning apparently tangible labors, products and possessions into ‘fluid and competitive’ phenomena of global financial marketplaces. Intellectually, ‘the furious proliferation of money talk in the media permeates the home to a degree difficult to imagine only a few years ago’ (37)

Martin makes a parallel between precarious lives and the global circulation of financial instruments through immaterial spaces beyond the regulatory reach of nation-states (much like the off-shore system of shell companies that allow wholesale tax avoidance). There is an accompanying sense, now familiar, of de-materialization, of work and everything else, imaginative consequence of life spent on-line. But the emphasis falls on the last line, on the proliferation of money talk and the observation that, even in 2002, it cascades from everywhere in volumes that were not always as they now are. With this, we enter familiar territory that we can explore at our leisure as this project evolves.

Van der Zwaan’s synthetic classification sits a top a great diversity of work. The Table of Contents for the Routledge International Guidebook to Financialization is a useful indicator of that work’s range and the names of (some of the) people who are doing it. The TOC is available here.

[1] On libertarian authoritarianism, beyond just looking around, see new work by Marlène Benquet and Théo Bourgeron on Brexit. An excerpt in English can be found here. A review(in French) of their recently published La finance autoritaire: Vers la fin du néoliberalisme is here.

[2] See his Chapter 12 “The Corporation Does Not Exist” and 13 “Police Theories of the Firm” pp.86-106.