Yale Model (Reading David Swensen) Part II

Demystifying Finance

Overview

The first part of this essay looked at the emergent space of active institutional investment management. This part looks at the Yale Model itself through the lens of its most well-known advertisement, David Swensen’s Pioneering Portfolio Management (PPM). It presents the model’s main features as well as those of the asset classes investment in which are among the model’s defining features. It is also interested in what holds the model together, in the long-term perspective as the basis for a worldview, in what that worldview foregrounds, and what it excludes. Swensen’s book captures a partial, particular view that takes itself as necessary and absolute in part because of the status it accords “the numbers,” the quantitative data central to the models’ approach to risk management. The main subtitles of this essay comprise a definition of an endowment: an organization; a portfolio, and a social network.

Reading Swensen II

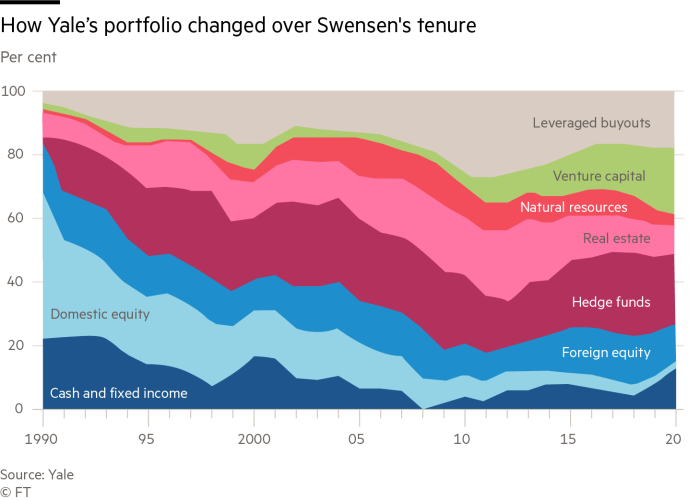

Those Returns

In 1989, Yale’s portfolio was invested conservatively, on the model laid out by Keynes: ¾ in stocks, bonds, and cash. By 2000, Yale was very little into stocks, not at all into bonds or cash and heavy into some new asset classes: private equity; hedge funds; real-estate investment trusts (REITs); commodities like timber; and non-US-listed equities. Collectively, these instruments were referred to as “alternative investments.” Alternatives to stocks and bonds, these asset classes were a way out of the loser’s game Charlie Ellis wrote about in 1975.[1] Alternatives and the Yale Model are central to the story of finance in the US from 1980. It was a period of quite radical transformation, one that passed through the stages represented in this graphic:

Source: World Economic Forum Report, “Direct Investing by Institutional Investors”

In this representation, alternatives are the main driver of change, with private equity and hedge funds chief among them. Yale had been in on alternatives for a decade prior to the book’s initial publication in 2000, and the money Swensen and his team directed into the sector played an important role in the latter’s development. There was a period during which the “golden age” of alternative investments and the model Yale developed moved in a tandem, and the returns stretched repertoires of adjectives.

The problems came later, in part because of the success of “the Yale Model.” By 2006, the effects of herding became clear. Vast amounts of institutional investor cash flowed into the hedge-fund and private-equity industries: arguably too much money, creating too much pressure in spaces with too few opportunities. Then came the financial crisis of 2008. As a sector, alternatives never really recovered. But this gets ahead of our story. In this essay, we want to read David Swensen’s Pioneering Portfolio Management in order to understand what the book’s acolytes in finance call its “philosophy of investing” and think about what holds it together as well as what it includes and, more importantly, what it excludes

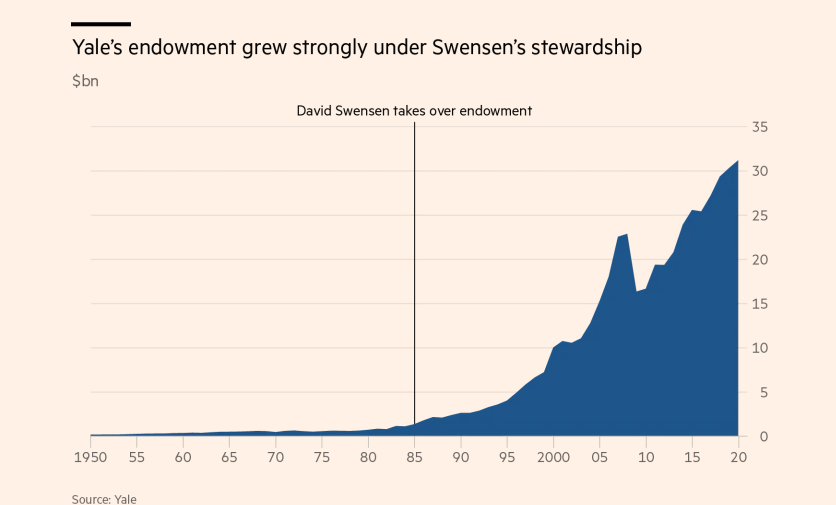

There is a tendency among those outside finance to intellectualize it, to imagine people like David Swensen (who was inside) to be motivated by finding elegant solutions to theoretical and ethical problems—but that world is mostly about the money, the returns on investment or ROI (also the French word for king). Those returns were the most talked-about aspect of “the Yale Model.” As the graphic below shows, those returns were consistently high over many years after Swensen became Yales Chief Investment Officer (CIO) in 1985. Those returns were proof of concept that papered over many sins. In his introductions to PPM, Charlie Ellis is effusive in expressing his admiration: those returns are splendid and lovely; exquisite and unparalleled. They brought luster to Yale, as well as to David Swensen, who, by all accounts, was otherwise merely a brilliant and affable fellow.[2]

Source: Financial Times Obituary “David Swensen, The Yale pioneer who reshaped investing” published 5/7/2021.

By 2000, endowments managed on the Keynes model were stuck with a strategy boring as watching paint dry that generated mediocre returns. It is easy to imagine managers of pension funds as well as of endowments being powerfully drawn to the exciting new world of finance theory and expanded asset allocations lit from above by the prospect of Yale-like returns (and performance bonuses). To read PPM is to take a tour of that exciting new world in the company of a narrative persona--named David Swensen---who outlines how he sees Yale’s endowment in both the institutional and finance-specific spaces in which it operates, extolling the importance of a “rigorous quantitative methodology,” dispensing all manner of advice about what the “curious” or “successful” investor might notice or wonder about with respect to risk management and its mirror image in portfolio diversification. He is frank about the fundamental importance of due diligence in evaluating and defining the asset classes a portfolio might take on. These definitions are qualitative, at the limits of number: Swensen emphasizes the importance of selecting “the best people” and cultivating relationships both within and beyond the endowment. The book conducts its tour and offers its advice as if to say: “Those returns follow from strategy and mindset rather than from me in particular. Develop the strategy, cultivate the mindset, create an excellent team and all this can be yours.” Except it took more than that, and Swensen knew as much—whence the stream of warnings: don’t try this at home and not everyplace is Yale. But PPM presents readers an image of how Yale’s endowment got those returns, and that is what many focused on, to the exclusion of Swensen’s warnings.

PPM can be roughly divided in two. The first part outlines the institutional space(s) occupied by Yale’s endowment. The second is more finance-facing. Throughout, the goal of active endowment management is to maximize returns on investment. When markets are efficient, Swensen was wont to say, and price approximates the underlying value of an asset, no-one is making any money. If you want to make money, Swensen tells us, you have to go to inefficient markets where there are informational asymmetries and pricing mismatches. You must go to private-finance markets. These markets come with considerable risk—but that risk can be managed using a “rigorous quantitative methodology,” one named means-variance with is a statistical package the endowment developed and used to manage its portfolio. Curiously, Swensen does not provide any technical information about means-variance, or links that readers might click through to find out about it, or an address from which one might purchase the software. In this sense, PPM presents an image of the Yale Model, one in which means-variance is a continuous reference-point and condition of possibility for the long-term perspective from which the narrator of PPM speaks.

Swensen focuses on portfolio diversification. The general idea is to divide the portfolio into five or six equal parts and to invest each part in an asset class. Every class is defined on the basis of its particular performance characteristics (asset characteristics, pricing history, etc.). The goal is to create a mix of these characteristics that balances them in a kind of machine of continuous, complicated contrary motions. A correctly balanced portfolio allows investment managers to set—and make--targets for returns while also hedging for risk. It is the old 60/40 stock/bonds idea in an expanded field.

As Swensen presents it, the central analytic work of an investment management team is to locate, assess, and “define” asset classes. The asset classes Yale defined are the focus in the book’s second part. He devotes particular attention to hedge funds and private equity. Lucrative but exceedingly expensive, private, illiquid, and opaque, these funds were central to Yale’s strategy. Reading PPM, one gets the sense that Swensen identifies most with hedge fund managers, those swashbuckling investors in speculative financial instruments, not unlike himself. By 2009 he had soured slightly on private equity because of the fees, particularly in cases where Yale could not come to side-letter arrangements that mitigated them (Swensen was famous for getting Yale sweetheart arrangements via side letter). These were the cases of “misaligned incentives” that Swensen complains about, misalignments not least because they insulted Swensen’s sense of Yale’s social power and the prerogatives that flowed from it. The opacity of private equity in particular shifted personal relationships and social connections to the forefront of due diligence and risk management.

The clarity of Swensen’s discussions of these asset types is basic to the book’s enduring popularity. He renders them accessible conceptually, and does so in a way that, while acknowledging the risks, reassures readers/managers that they can be managed, from a long-term perspective.

PPM also suffused with an implicit ideology or worldview, one particular not just to endowment managers but to contemporary finance in general. Teasing out that ideology is the main task of this essay. It emerges through themes that include beliefs about number and the kind and status of information about the world it imparts; about elite communities and how they regard themselves and how they see—or do not see—the world outside themselves. In private finance in particular, power is the power to be invisible to the outside. The essay argues that the appeal of Swensen’s “philosophy of investment management” lay not only in its explicit content, but in the ways in which it updates not just the figure of the active investment manager, but basic elements of the ideology that underpins contemporary finance, one that we think explains and reinforces an autocratic style of management, on the one hand, and oligarchy, on the other.

With this dual focus in mind, the rest of this essay moves through Swensen’s image of the Yale Model. It is organized under rubrics that are also defining characteristics of an endowment: An Endowment is an Organization; An Endowment is a Portfolio, and An Endowment is a Network (Mondo Chad).

An endowment is an organization

The David Swensen of 2000 or 2009, the one that readers meet in PPM, had already played a important role in redefining active institutional investment management. He did this as the Chief Investment Officer for Yale University’s endowment, a position to which he was appointed in 1985. He was also a believer: in Yale; in its educational mission. He saw the endowment’s primary role in supporting the educational mission, and that provided him a sense of higher purpose, something admirable and beyond himself, on behalf of which he could be ruthless and that ethically justified pursuit of those returns. He enjoyed, and used, Yale’s status. As a person, Swensen was an active participant in its culture. He taught courses on institutional investment strategies at Yale’s School of Management through which passed many MBA students who were following the ideal-typical finance trajectory from a job at an I-bank out of college, a three-year apprenticeship, a prestigious MBA, and a job in private equity.[3] Swensen was an important mentor to those hired to work for the endowment as well. The internal organization of the endowment was amenable to mentorship: a mostly horizontal space with an internal culture that he would describe in interviews as like a seminar. It helped to be interested in sports and to join the other bros for cards on Wednesday night. Former students and colleagues formed an inner circle among the broader network of Yale alumni with careers in hedge funds and private equity.

Reflecting the academic environment in which the endowment operated, Swensen foregrounds just how interesting he and his colleagues find “the universe of financial instruments,” saying that they would be willing to work for free in pursuit of their interests in order to “mine the handful of gems from the tons of mine ore.” (p. 3) But they didn’t have to. (At a thematic level, Swensen’s emphasis on how the extent of his team’s engagement with the universe of financial instruments attests to the quality of the endowment’s asset-class definitions which inform means-variance without being informed by it). Swensen saw Yale’s endowment corporation as a community of talented, interested, and interesting people who brought to their roles a “knowledge base that knows no bounds.” In his view, active investment management was, ultimately, a humanistic undertaking: “A deep understanding of human psychology, a reasonable appreciation of portfolio theory, a deep awareness of history and broad exposure to current events all contribute to the development of well-informed portfolio strategies.” (3)[4]

Swensen earned a doctorate in economics at Yale in 1980. He wrote a dissertation on corporate bonds pricing under the supervision of the economist James Tobin. Tobin’s influence was key. On the one hand, Tobin was a long-time advocate for the professionalization of institutional investment management and the integration of MPT into how portfolios were structured; on the other, his personal influence was fundamental in getting Swensen the position as Yale’s CIO in 1985, despite his relative youth and lack of experience.[5]

After finishing his dissertation, Swensen worked for Salomon Brothers, where he was part of the team that structured the first interest-rate swap.[6]

Swensen’s arrival as CIO was not accompanied by an immediate transformation of how the endowment operated--in 1989 the university’s holdings were still ¾ in stocks, bonds, and cash. But Swensen and Takahasi were using their means-variance statistical package by 1986. We’ll talk more extensively about means-variance and portfolio diversification in the next section. But here, we note that the methodology was basic to changing the time-horizon in which institutional investment management happened.

In PPM, Swensen argues that Yale’s endowment supports the university’s mission with a “time-horizon of centuries” so its management must devise long-term strategies as well. We saw in part one of this essay that the more traditional investment strategy of stock-picking operated with an exceedingly short time-horizon. The problem Ellis posed in 1975 was: how to move beyond that very short time-horizon, that presentism. Ellis recommended turning away from price and toward risk and how to manage it. This pointed toward the space Swensen would later come to occupy as a matter of everyday practice (running the endowment) and that he was later able to transpose into a narrative viewpoint in PPM, one anchored in the long-term. But what does such a long-term perspective look like?

Any endowment operates in an institutional setting comprised of multiple time-horizons, so it stands to reason, in principle, that an endowment working with a long-term perspective can and will encounter tensions with other parts of the institution and that these tensions will require a balancing of interests. Maybe this is why Swensen’s narrator dislikes things that might put him in a reactive position. He is not inclined to allow the endowment to respond to unexpected shortfalls in university revenues or operating budgets, or to pressure that might arise to increase the endowment’s contributions to student financial aid because of the publicity that often attended the endowment’s returns (Swensen refers to the idea as “trading today’s students against tomorrow’s”). Swensen sees the endowment as supporting the university’s mission in ways that are symmetrical with the longer-run through specified funding for aspects of university operating budgets, the maintenance of long-term commitments that follow from donor restrictions on gifts (keeping endowed chairs funded in perpetuity, for example).[7]

In other words, the endowment is not a “rainy-day fund.” Rather, Swensen argues, the endowment pursues predictable and increasing returns in a quest for autonomy relative to both alumni gifts[8] and government aid. Writing in libertarian, as he often did, Swensen saw government aid as coming “with strings” that amount to “a demand for a say in endowment governance.” The autonomy bought by the endowment’s ROI reflected and supported the excellence of Yale as a whole, both directly in support for teaching and research, and more generally, as an indicator of the university’s relative status among competing institutions. Endowment size is vastly more important than any use to which it might be put in the prestige metrics published by US News and World Report (pp, 17-9).[9]

Swensen connects the endowment’s “time horizon measured in centuries” to the centrality of the kind of “long-term institutional commitments” particular to colleges and universities. He writes, without irony—this was a different time--that tenure is such a commitment. (p. 9). But, like all of us, David Swensen was mired in the flux of experience in everyday life and its variable relations to time. Martin Heidegger valued boredom because it made the temporality of everyday life explicit—but no-one is bored all the time. Everyday life is a variety of relations to time, very few of which are long-term in the sense Swensen gives the expression. It is not obvious what such a long-term perspective might look like or how one might come to occupy or inhabit such a perspective.

Swensen considered “a rigorous quantitative methodology” to be the backbone of such a perspective, but it’s more accurate to see the experience of working with such a methodology as more fundamental. This is not a new insight: the final paragraphs of Blaise Pascal’s “The Wager,” a famous passage from his Pensées, address the situation of an interlocutor who has been presented a probabilistic argument for belief in God. That’s all fine, he says, but I am so constructed that I still cannot believe: what then should I do? The narrator responds: keep to rituals and discipline the passions. Over time, repletion alters habits, and the alteration of habits will, eventually, bring you to belief--or to forgetting that you don’t. Practice, repeated over time, can transform one’s viewpoint. Interaction with ideological, material, professional, and political habits alike, can, over time, constitute a kind of space one can inhabit that refigures how one projects the world and one’s place within it. Professional life is a self-conditioning, through which one comes to take over a skill set and the accompanying perspective or viewpoint, becoming like a tennis player able to drop shots with precision. Hierarchy and pressure to conform facilitate the taking on of such ideologically problematic dimensions as may obtain, particularly where they comprise a kind of substrate, spoken but not spoken-about, a lingua franca (agency theory, conservative libertarianism) so long as they do not interfere with backhand returns and types of spin. But Swensen does not work on such a meta-register. For him, the hallmarks of having assimilated the long term were pragmatic, not-reacting to bull or bear market conditions, to turbulence or price movements. Instead, one acts by the numbers. Over time one may reach a Swensen level of mastery of the long-term perspective and write a book that is narrated from it.

Swensen’s work on corporate bond pricing and structuring of swaps may have given him a leg up in the above. He brought a particularly modern understanding of debt to a very traditional areas in which endowments had been invested. In the beginning there was real estate and fixed-income securities (bonds) and prudent endowments invested in them both. The long-term was simple: one held a piece of real-estate until it was sold and held bonds to maturity. After Keynes, endowments expanded their holdings to include stocks, and that added some complexity to bonds by diversifying how they could be held - for themselves, but also to hedge or offset risk because bond prices usually move counter-cyclically. Hedging presupposes that one might sell prior to maturity in a secondary market—but this option did not significantly transform bond markets or how endowments used bonds. Most bonds are held to maturity. Equities are much more active.[10]

David Swensen’s specific background positioned him well to upend all that. One of the bigger transformations of the 1980s was in the use of high-risk corporate bonds, or junk bonds, by private-equity shops like KKR to fund “leveraged buyouts” (acquisitions financed using debt). At the time, the finance press packaged this as conceptually problematic (creating money out of thin air), a matter of great complexity and dubious ethics. Swensen was in a position to understand what was going on at the level of junk bond pricing and not only not be put off by it, but to see the newly rebranded private equity as a potentially lucrative space for Yale.[11] More generally, bond pricing is by its nature future-oriented. Relative to equities, bonds do not trade much. Someone who thinks about finance via debt and/or debt-based instruments would likely be more comfortable with illiquidity than would be someone steeped in equities.

Swensen came to Yale able to see the transformations in the usages of debt across the 80s and 90s and be comfortable with them. Swensen saw himself as understanding how returns are really produced whereas the others, the market gurus, with their outmoded skillsets, did not. Returns are produced via increasing risk exposures “beyond markets” into private-finance spaces despite their opacity and irrationality. Whence the need for “a rigorous quantitative methodology” to manage it.

Swensen wrote about all that with clarity and serenity. PPM made the idea that an endowment or pension-fund would take on considerable risks entailed by a reach for yield seem not-crazy. Also, those returns.

An endowment is a portfolio

Swensen and Takahashi’s central innovation was to manage the Yale endowment’s portfolio on the basis of modern portfolio theory. A 2005 article published in Yale’s alumni magazine included the following assessment from other advisors:

In retrospect, Swensen's approach sounds sensible, but at the time it was revolutionary. "No institutions were managing money in accordance with what finance theory would tell us," he says. "It just wasn't done." Len Baker '64, a Silicon Valley venture capitalist and member of the Yale Corporation, says that one of Swensen's strengths is his willingness to think for himself. "He doesn't get his information from consensus," Baker says. "He does his own thing." Having his trusted friend Takahashi at his side helps a lot; they enjoy challenging each other's ideas, as well as upending conventional wisdom. "They do a lot of introspection," says Josh Lerner, a Harvard Business School professor who wrote about Yale's methods for an HBS case study. "And they have the self-confidence to chart a distinctive path."[12]

These comments indicate something of the work that lay behind the narrative perspective readers encounter in PPM, the extent to which it was a break with then-conventional wisdom--and of how unusual were finance people willing or able to make such a break. Finance is not full of mavericks.

Modern Portfolio Theory (MPT) is based on portfolio diversification. Diversification requires a portfolio be divided into five or six equivalent parts, each of which invests in a particular asset class. Every asset class is defined by its characteristics and price history. The juxtaposition of asset classes makes the portfolio into a kind of machine in continuous, complex contrary motion. These relationships are monitored by quantitative means, and the numbers determine when a “rebalancing” is required—and not unexpected price fluctuations or other present-oriented datapoints. For Swensen, this quantitative methodology is the most important single feature of the Yale Model and its long-term investment perspective, and thinking about finance through the methodology’s lens imparts a special kind of insight:

Market participants rarely wonder whether high returns come from accepting greater than market risk. The investment community’s lack of curiosity about the source and character of superior returns causes strange characters to be elevated to market guru status. (pp. 246-7)

But those returns, from before Swensen’s book came out and before the period between July 2000 and June 2003 during which “the S&P 500 fell 33% while the Yale Endowment fund gained 20%.,” those returns made the risk that accompanied moving into an expanded field of asset types seem manageable--as did PPM. Together, they explain why there is a Yale Model.

Swensen and Takahashi named means-variance as a tribute to James Tobin. As we noted earlier, Tobin was a long-time advocate of integrating Modern Portfolio Theory into how institutional investors run their portfolios. The notion of diversification and its underlying mathematics were initially presented by Harry Markowitz in his paper “Portfolio Selection” which was published in the March 1952 issue of The Journal of Finance.[13] Before Swensen and Takahashi created an automated application for MPT, there had been a small cadre of financial analysts that understood the implications of MPT and who were able to see how it might transform institutional investment. Many of these analysts were associated with the CFA Institute’s Financial Analysts Journal. In that context, it seemed like MPT had been conjured to resolve problems that writers for the journal had been pointing since the late 1940s: the biggest problem for the future of institutional investment management lay in “overcoming investor psychology” and some form of quantitative methodology was likely the way to manage the feat,[14] Over the ensuing decades, an extensive conversation grew up around MPT. Charlie Ellis’ essay “Loser’s Game” was part of it.

The mathematics in Markowitz’s paper were complex and cumbersome to work with manually. Applications were therefore limited and MPT remained theoretical. In the mid-1980s, Swensen and Takahashi took advantage of the contemporary computing capacity and processing speed and were among the first to automate MPT.[15] The resulting means-variance has since itself become an object, but in the finance history of finance written by people in academic Finance Departments on the assumption that progress itself can be measured by the spread of quantitative approaches of the kinds valued in finance and economics departments, both in the finance industry and the world. More recently, some historians have pushed back:

It is usually argued that not until Markowitz’ paper on [portfolio] diversification in 1952[16], and in practice not until the advent of fast computers in the 1970s, were these modern approaches to portfolio management fully implemented. Prior to this, investors are thought to have had an erroneous and unsophisticated approach to risk and return despite the fact that some might have been diversifying their portfolios in practice.[17]

In the US, many college or university endowments with portfolio holdings valued at less than $1 billion are managed in keeping with Keynes’ model----commentary that equates quantification with progress would see them as relics of an amateurish past. Such a perspective would also not be inclined to take account of the trade-offs that accompany adopting an approach like the Yale Model.[18] Many of the language games preferred by contemporary management literature rely on similar moves.

But, despite all the talk about the centrality of means-variance, Swensen provides very little technical information about it in PPM. By the time he wrote the book, means-variance seems to have become an important but routine aspect of managing Yale’s endowment, a software package that produced a steady stream of data amenable to interpretation by users with “a reasonable appreciation of finance theory.” But should you, reader, be interested in the mathematics, an introduction is available here.

Asset Allocation

Portfolio management using means-variance has two basic components: asset allocation and rebalancing. Asset allocation refers to the range of asset types in which the endowment would invest its five or six subdivisions. Yale considered changes to asset allocation once a year.[19] Swensen describes the process as it took place in a seminar: analysts present the results of their research, their definitions of a given asset class when the financial instrument type was new, and made a case for or against its inclusion in Yale’s portfolio.

Rebalancing, the buying or selling of asset types already in the portfolio, happened when the numbers deemed it necessary. [20]

Asset-class definition of is one of the limits to the Yale Model’s penchant for quantification. Definitions are the work of analysts who collect industry characteristics, vehicle’s properties, asset price history, and so on in order to isolate of the characteristics that enable future price trends to be fashioned probabilistically. These definitions precede and condition means-variance quantitative analysis. As the current strategy page for Yale’s endowment puts it:

Because investment management involves as much art as science, qualitative considerations play an extremely important role in portfolio decisions. The definition of an asset class is quite subjective, requiring precise distinctions where none exist.

The website continues:

Returns and correlations are difficult to forecast. Historical data provide a guide, but must be modified to recognize structural changes and compensate for anomalous periods. Quantitative measures have difficulty incorporating factors such as market liquidity or the influence of significant, low-probability events. In spite of the operational challenges, the rigor required in conducting mean-variance analysis brings an important element of discipline to the asset allocation process.

The problem here is an old one: axioms cannot be demonstrated by a proof that presupposes them.

Swensen tried to make some of the above concrete in interviews with Yale Alumni Magazine. He gave one in 2009 in part to promote his second book, which was directed at retail investors. Swensen explained the basic importance of asset allocation to his thinking and contrasted it with strategies centered on price. But note in what follows that Swensen points to the roles played by investment fees as an important differentiation of institutional from retail investors. For retail investors, fees are a drag on earnings. For institutional investors, they are a cost of doing business. Institutional investment managers do not manage their own money. Many have no idea know how much their funds pay in fees to private equity, for example.[21] The interview:

Y: Explain this idea of asset allocation, please.

S: Asset allocation is the tool that you use to determine the risk and return characteristics of your portfolio. It's overwhelmingly important in terms of the results you achieve. In fact, studies show that asset allocation is responsible for more than 100 percent of the positive returns generated by investors.

Y: How can that be?

S: It's because the other two factors, security selection and market timing, are a net negative. That's not surprising. They're what economists would call zero-sum games. If somebody wins by buying Microsoft, then there has to be a loser on the other side who sold Microsoft. If it were free to trade Microsoft, the amount by which the winner wins would equal the amount by which the loser loses. But it's not free. It costs money. It costs money in the form of market impact and commissions if you're trading for your own account, and it costs money in terms of paying fancy fees if you are relying upon an investment advisor or mutual fund to make these security-specific decisions. For the community as a whole, all those fees are a drag on returns.

That's why the most sensible approach is to come up with specific asset allocation targets that you can implement with low-cost, passively managed index funds and rebalance regularly. You'll end up beating the overwhelming majority of participants in the financial markets.[22]

There is a more expansive discussion of the endowment’s approach to asset allocation in the 2005 article “Yale’s $8 Billion Man”:

The heart of the endowment manager's job is to allocate assets to different classes of investments. In the early 1980s, Yale held more than three-quarters of its money in U.S. stocks, bonds, and cash. This was a mistake, Swensen and Takahashi decided; the analytical tools Swensen had learned as a graduate student indicated that the portfolio was not sufficiently diversified. (Tobin used to explain portfolio theory by saying it boiled down to "Don't put your eggs in one basket.") By putting too much money into U.S. stocks and bonds, Yale was both taking on too much risk and missing out on opportunities in such investment classes as foreign stocks; real assets, which include real estate, oil and gas, and timber; private equity, which includes venture capital and buyout firms; and a category known as "absolute return," hedge funds that try to capitalize on market inefficiencies and special situations such as distressed businesses. As Swensen explains it, those other asset classes deliver "equity-like" returns, but because they are not correlated with U.S. equities, they cushion the portfolio against losses when the stock market goes through its inevitable down cycles.

How diversified have Yale's holdings become? Over the years, the endowment has invested in public companies like the cable giant Comcast and the insurance firm UnitedHealthcare, startups like Cisco, Yahoo, and Amazon before they went public, newly privatized firms in Russia and small companies in China, high-end office buildings such as the John Hancock Center in Chicago, timberland in Maine and Idaho, even a resort in Tucson. (The women's golf team got to practice there for free one year.) Most recently, according to the Wall Street Journal, Yale took a big stake in the Kimpton Hotel and Restaurant Group, a fast-growing chain of hip boutique hotels, many of which operate under the Hotel Monaco brand. By diversifying beyond U.S. stocks, which are widely followed, Swensen has been able to seek opportunities in less liquid, less efficient markets where the sophisticated investment managers that he hires could gain a competitive advantage. [23]

Alternative Investments

The interviews quoted above give an idea of Yale’s expanded range of asset types: foreign equities; real-estate; timber; energy; alternatives. This section focuses on hedge funds and private equity in particular in terms of how the David Swensen who narratives PPM sees or presents them, which is as interesting for what it leaves out as for what it includes. We proceed in this way because there’s a sense in which Swensen is indirectly selling these asset types with his calm and lucid descriptions, in a way similar to how he sells portfolio diversification and means-variance as an approach to risk management adequate to an expanded range of asset types that includes them. We want to understand something of how Swensen made these assets seductive even as we know that, at bottom, it’s those returns.

Yale was known not just for its expanded field of asset classes, but also for its definitions of alternatives (definition is used here in the database sense, to denote their inclusion). When Yale first defined hedge funds in the early 1990s, it was the first endowment to invest in the industry. Yale was in private equity soon thereafter. David Swensen looked at alts through the prism of the endowment’s definition (referring here to defining characteristics). As the name implies, hedge funds make countercyclical bets: the overall dynamics of this asset-class resemble those of bonds, but without being tied to bond markets and with much better returns. Swensen particularly admired long-short strategies that took countervailing positions on securities in order to “eliminate the market” and thereby amplify price gains or losses, making money either way.

While there are several strategies in the private equity sector, for Yale the important ones are leveraged buyout funds and venture capital. Of the two, Swensen preferred the LBO funds because they pursued strategies that clearly separated PE from other asset types, moving generally like equities but without being linked to the stock market. LBO funds also offered spectacular windfalls. For Swensen, venture capital was more like other types of company, which means that VC funds offered few diversification advantages that might justify their expense and risk.

What else did Swensen see? He saw the private, secretive, often ruthless HF/PE sectors as spaces in which a well-connected active manager could make a lot of money---in this case for Yale, which made making a lot of money a very good thing indeed.[24] The reason such money could be made is that the markets are inefficient. As he put it: “Sensible active managers prefer markets with inefficiently priced assets and avoid markets with efficiently priced assets.” (p. 73). In other words, where markets are efficient, no-one is making any money. This is very far from libertarian notions about efficient markets - price as a sum of best socially available information and any political derivations that might be made on their basis. Investment managers are active, they’re out to maximize returns; libertarians are contemplative and incline to metaphysics. We are also far from the idea that financial markets can be understood on the model of the village economies preferred by neoclassical economics. Perhaps these distances point to an ideological function that Jim Cramer might serve, to reassure conservative libertarians that they can continue projecting their particular “world of finance.”

Sensible investors, then, prefer inefficient markets where assets can be had for less than their fair value. With private equity and hedge funds, the inefficient markets in which Yale invests are private. Information can be a problem because there are no rules about disclosures because there is no general public of investors to protect and no illusion of equality to be maintained. A sensible investor, looking to maximize returns, would be drawn to private, for-the-most-part unregulated funds. Where in public market offerings there would be documentation available for potential investors to use in getting a sense of the financial well-being of the underlying company, in private finance there is often very little documented and access to it is uneven. What matters most is access, edge, inside information, the stuff on which finance actually turns, even as it skirts the edge of legality (whence Matt Levine’s quip “Everything is securities fraud.”). [25]

Sensible investors rely on social connections, word of mouth, friends and friends of friends, in part by necessity as these funds are not allowed to advertise. In this there is a residuum of the 3c1 exemption from the Investment Advisor Act of 1940 that was carved out at the time by powerful and wealthy individuals who looked to exempt their own advisors from disclosure requirements and thereby protect their privileged positions. Hedge funds and, later, private equity were grandfathered into the 3c1 exemption. Yale would enjoy tremendous advantages even had David Swensen not been an active mentor and teacher because of its alumni networks and location in the part of Connecticut that is also central to the geographies of both hedge funds and private equity. But as he was, he would not just identity the better active managers in hedge funds or private equity: he likely knew them, and they him, or at least of him.

When communication between endowment and fund managers were lubricated in such ways, Swensen would enjoy advantages that most other sensible investors might lack. Yale could rely on continuous access to top decile (20%) private equity funds. The importance of these funds has increased as private equity has been flooded with investor money because, as Jeffrey Hooke shows in The Myth of Private Equity, only the top decile matches or beats the market, Competition among investors is intense. There’s nothing remotely fair about it--but sensible investors prefer that. Plus, there was, and still is, an enormous amount of money sloshing about in alternatives. SEC Chair Gary Gensler provided the following numbers in a November 2021 speech:

Why do these funds matter? They matter because they’re large, and they’re growing in size, complexity, and number. Altogether, U.S. private funds have gross assets under management of $17 trillion with net assets of $11.5 trillion. The sheer size and transaction activities of these funds represent a critical portion of our overall capital markets. Hedge funds have gross assets of at least $8.8 trillion and net assets valued at about $4.7 trillion. Private equity funds gross assets of $4.7 trillion and net assets of $4.2 trillion.

Politically, the people in finance are not of one mind: not everyone shares the libertarian paranoid-reductive view of government and regulation. Many see regulation as a necessary and important part of the system, one that, if properly implemented, can assure that extraction has a future. Swensen was in the latter group. In a 2009 interview Swensen argued that the scale of private funds posed a systemic risk and that it was “crazy” that there had been no move to regulate them, particularly after the 1989 implosion of the hedge fund Long Term Capital Management nearly imploded the entire financial system. He speculated that the explanation lay with the fact that, in 1989 the system bounced back quickly as it had after the 1987 stock market crash. After the 2008 financial crisis, Swensen said he was “cautiously optimistic that we will have some sensible regulatory reforms prompted by this economic and financial crisis. Of course, the devil's in the details.” Until that time, Yale stayed in hedge funds and private equity because, in the long run, the numbers said outsized returns justified the risk exposures and fees.

What else did he see when he looked at alternative investments? He saw active investment managers like himself. With hedge funds in particular, Swensen sees a pure form of active management, without which “absolute returns” would not exist” (182). He admires their strategic innovativeness and simplicity of their design, not least because that facilitates asset-class definition and evaluating fund performance. Managers either “add value” (they generate returns in excess of fees) or they do not. Typically, hedge funds lock up investor capital for around 4 years, which is relatively short when compared with the private-equity average of 12 years, and are in general more open to allowing investors earlier redemption or exit options at intervals before that. Private equity typically does not offer early redemption options.

Swensen does not discuss hedge funds as a class in general. Instead, he focuses on particular strategies, tied to particular managers that he does not name (another of the ways in which PPM provides an image of how things work at Yale’s endowment). He singles out two strategies: event-driven, and value-driven aka long-short. Both look to exploit irrationalities in asset pricing. Event-driven strategies often involve buyouts of companies where value-driven/long-short strategies work with financial instruments. Swensen sees event-driven strategies as research intensive and rooted in knowledge of “complex corners of the investment opportunity set, an area often avoided by mainstream analysts.” Long-short strategies “attempt to add value by identifying over- and under-valued securities, creating portfolios with roughly off-setting long and short market exposures.” Again, for asset-class definition purposes, what matters about each strategy is its distinctiveness, which informs that strategy’s utility for portfolio diversification. Swensen admires the skill of hedge-fund managers. These funds, he writes:

…appeals to investors who believe that providing funds to superior managers operating with few constraints will lead to impressive investment results regardless of the upswings or downswings of traditional marketable securities (193).

In other words, they deliver returns on target.

But Swensen is not blind to sector problems. Hedge funds are opaque so, for any particular fund, risk assessment is a problem. Sectoral performance can be hard to asses because “industry purveyors of statistics” circulate “rosy pictures” that are “wildly at odds with reality.” Hedge fund valuations are unreliable except as marketing devices for new funds, but hedge funds’ relatively short capital lock-ups mean that it more possible than to distinguish realized returns, net of fees, from accounting projections like internal rates of return than is the case with private equity. Swensen notes that it is very difficult, even for Yale, to locate “a group of exceedingly skilled investment managers” whose “value-adds” can consistently “overcome rich fee arrangements”---as with private equity, a base of 2% of the total capital invested and 20% of performance fee taken out of returns that exceed an agreed-upon benchmark plus other management fees and incentives—which amounts to a “misalignment of interests” between general and limited partners, fund managers and investors. The fees work to “incentivize” fund managers to enrich themselves at the expense of investors, even when social connections might link endowment and fund managers. For all these reasons, Swensen concludes that, while a portfolio of carefully chosen hedge fund managers can deliver “impressive investment results” the construction of such a portfolio should left to “sophisticated investors” (here in the conventional sense of knowledgeable) able to “commit significant resources to the manager evaluation process.” (199) “Casual approaches lead to almost certain disappointment.” (198).

Yale was among the first endowments to invest in hedge funds. Not long after, they also went in on private equity, but, by the 2009 edition of PPM. Swensen seems to have soured on the asset class. PE promised outsized returns and, since 2006, they failed to deliver. PE LBO funds lock-up of investor capital for 10-12 years, which is long enough to create problems of distinguishing realized returns from accounting projections like IRR that go beyond those indicated above for hedge funds. PE valuations are suspect and its shares illiquid. Risk is both very high and not amenable to quantification within the means-variance framework. Private equity charges “rich fees” which of course Swenson calls “a misalignment of interests.” Here again, Swenson prefers discussing specific strategies to the sector as a whole. In this case, he looks at LBO funds, particularly those that “engage in significant operational changes” in acquired companies because the simple use of leverage (debt) to fund a buyout is not adequate to distinguish LBOs from corporate mergers and acquisitions.[26] Swensen writes that private equity LBOs become distinctive when their managers reorganize their companies, when they “impose discipline”:

Separation of ownership (by shareholders) from control (by management) results in a substantial gap between the interests of shareholders and the actions of management. Over-the-top offices, excessive salaries, bloated fleets of airplanes and other unjustified managerial perquisites rarely enter the picture in profit-oriented private investments. (220)

Agency Theory (Ideological Substrate)

Swensen’s viewpoint on the type of “discipline” that private-equity imposes is a re-statement of a bowdlerized agency theory. It informs the rhetoric of incentives as well. In the above, Swensen spices things up with a details that might have been pulled from Barbarians at the Gate in “the bloated fleets of airplanes” could refer to the planes used by Nabisco’s CEO to fly his German Shepard from place to place that the book made over into a symbol of the corporate excess of the Bad Old Days that old-school private equity funds were jockeying to discipline away, only to find themselves blindsided by KKR with its novel funding arrangements based in junk bonds.

Agency theory was spelled out by Harvard Business School’s Michael Jensen. It is based on a libertarian understanding of private property ownership that centers on control, which it then projects as an imaginary map of a company or firm. It was developed as a counter Adolf Berle and Gardiner Means’ 1932 book The Modern Corporation and Private Property, particularly the descriptive claim that, in large-scale corporate manufacturing, ownership and management were separated and that effective control over production was exercised by management and trade unions and not by shareholders. For libertarians committed to equating ownership with control, this was horrible, and needed to be wished away.

Imagine a diagram of factory that includes trade unions and, by extension, working people. Agency theory fundamentally alters that diagram. In the new one, shareholders own the company: control is exercised via the imposition on the owned company of an ethical obligation to maximize their returns; shareholder interests are represented by The Board; CEO and CFO find themselves between shareholders and the representatives and management. For agency theory, they need to be incentivized to act in shareholder interests and maximize their returns. Remuneration is the way to do that: agency theory is the theoretical justification for corporations buying back their own stock. In a correctly organized company, then, CEO and CFO compensation are tied to share price. Management is framed as self-serving and unruly, open to motives other than maximizing shareholder return on the one hand while being difficult to incentivize on the other. They are in need of discipline, a discipline imposed by the streamlining of organization, optimizing of processes, imposition of efficiencies, and elimination of waste in the sense of factors that do not maximize shareholder returns like stable jobs with benefits for working people. Agency theory makes outsourcing of labor seem reasonable: it reduces salaries and offloads benefits; by eliminating secure employment trajectories it also ends pension obligations. How does agency theory account for the consequences of the imposition of discipline? It doesn’t. Labor is simply a variable cost. This is evident in the cognitive map of the firm on agency theory. Management is the outer edge of the meaningful world. Beyond them, moving away from shareholders, there is nothing: no workers; no communities. What happens there where there isn’t counted, so what happens there doesn’t count.

Agency theory is presented in university finance department curricula, particularly at the MBA level, as if it were an adequate map of the meaningful world. Introductions to Finance treat it as factual and they test that students have internalized it in exams. It is the justification of every LBO, no matter the fiasco that ensues. That agency theory is treated as though it informs pictures of the world that are even a remotely accurate is remarkable enough. But even more remarkable is the destruction it has enabled and continues to enable, from the deindustrialization of America beginning in the mid-1970s to the problems in private-equity-owned healthcare today.[27] Still more remarkable is the destruction is its invisibility. Agency theory dissolves real-world, extra-financial consequences to finance-based actions.

When David Swensen looks at alternatives, or at the Yale’s endowment and the social network of which it is part, along the horizontal of his own class position, what he sees is differentiated and his perceptions are lucid. But when he looks down the vertical of class (and, at least in PPM, he almost never does) Swensen sees ideological projections and recapitulates them without a trace of self-awareness.

An endowment is a network (Mondo Chad)

In early 18th century France, the Duc de Saint-Simon found himself exposed, on the wrong side of a factional struggle in the court of Louis XIV, and was exiled to his chateau. From a very ancient aristocratic family, the Duc fumed that he had been treated with such insolence by more powerful courtiers from less prestigious families. He vented his anger into his diaries in which the Duc looked to destroy the court that had treated him ill in the only way available to him: to demystify it, expose its underlying rules and foreground the petty venality of court society. For example, he showed that, behind the Sun King iconography, Louis XIV, a mediocrity personally and intellectually, was as much prisoner as master of the highly ritualized social machinery of his court. The Duc de Saint-Simon did not manage actually to destroy the French court, but the diaries of his efforts were, much later, an invaluable source for historical sociologist Norbert Elias’ excellent book The Court Society, in which he uses them to tease out a picture of the underlying rationality of aristocratic life in Louis XIV’s France.

David Swensen is nothing like the Duc de Saint-Simon. He is neither exiled nor aggrieved. Quite the contrary, in PPM he is the center of a kind of court held together not by blood but by status and money. Swensen does not set out to demystify by exposing the underlying rules of the social game of endowment management. Rather, PPM demonstrates his mastery of those rules: he talks through rather than about them, more La Rochefoucald than Saint-Simon. His discussion of the investment process is an approximate map of the Yale endowment as a network. He shows that there is a geography, but does not name its non-institutional features nor does he describe them in any detail. Neither jockeying for position nor venality gets exposed.

The David Swensen we experience in PPM thinks of a hedge fund or a private equity fund as an example of a given asset class and as a strategy. But he also thinks in terms of particular (active) managers. He takes the partnership arrangements that link the endowment (limited) to fund managers (general) seriously but in ways that give no hint of the adversarial character of most limited partner agreements that we know about. At times, Swensen gives the impression that the boundaries that distinguish the endowment from its partners are porous. He seems to identify with the skill displayed by “top decile” hedge fund managers: he admires their freedom and how swashbuckling they are.

The networks that linked Yale to its hedge fund and private-equity partners were the terrain on which Swensen and his colleagues hunted edge, inside information, privately shared, access to which is fundamental to active management. Swensen characterizes such access as a result of his fund’s due diligence, and advises the reader that such diligence can only be carried out where there are resources adequate to support it. Without them, he says, active investment managers would be better off avoiding these assets. (294-6) But Swensen also makes it clear that any sense of identification with his partners he might express, any sense of organizational porosity that might accompany them, was underpinned by “deal structures” (limited-partner agreements) and the degree to which they created “interest alignments” (fees and other arrangements, usually worked out in “side letters”) that worked to Yale’s advantage (295). He is quite harsh in his criticisms of outfits like KKR who refused, for whatever reason, to give Swensen the concessions he felt due to him---or, rather, to Yale. Rightly, but with motivation, he complains about KKR’s “unbelievable greed.” (pp. 287ff). Elsewhere he rails against the hedge fund JMB’s “unjust fee bonanza” (291-2).

In Swensen’s approximate geography of the Yale endowment, the boundary that separates inside and outside and its features are made of contracts and side letters. On the inside is a space of proximity, of collaboration and information exchange both about what is happening both within and without. The inside/outside distinction, operative but subject to revision, did not separate belligerents, except where the obnoxiousness or failure to deliver set this or that entity apart as definitely not OK.

The whole of this tiny universe was, is, and remains invisible to outsiders.

Swensen was the opposite of an outsider. He worked in a closed community, advantageously located geographically, institutionally and socially, among friends, former students, endowment advisors, and the myriad connections made possible by them, networks within networks that were fundamental to Yale’s successes. But here too is only an approximate geography: Swensen describes the spaces in which he operates at a slight remove, emphasizing the importance of choosing the best, most appropriate investment partners. Charlie Ellis considers choosing people to work with one of Swensen’s deepest talents. At the same time, while the array of “outsourced active managers” was as—or more—important to Yale’s returns, accounting for 60%, as was the quantitatively driven asset allocation process (40%), in PPM, it is the allocation process that gets the detailed presentation. Descriptions of the allocation process bring out the focused serenity characteristic of his writing across much of the book, a serenity of a piece with his occupation of a different temporality, one at a remove from the present and resistant to reactiveness. If one frames it with reference to those returns, Swensen’s style becomes a kind of aesthetic justification for the Yale Model, allowing readers of PPM to imagine (or flatter themselves into seeing) it as an introduction to a kind of glass bead game---and this also points to the elite status of the networks and that, in turn, can be seen as an explanation for PPMs approximate geography. The creation and cultivation of social networks among the well-connected with an eye toward enhancing returns is hardly an innovation in finance, quite the contrary: it’s how the game works. But here, as everywhere else, not all networks are equal and not all endowments are Yale.

Swensen’s sketch of the investment process walks the reader through some of the organizational features of an endowment that connect it to the finance world beyond itself (297-344). There are the outsourced intermediaries: the pooled investment vehicles like funds of funds, which Swensen thinks are too expensive; the consultants whom Swensen finds sell the same advice to everybody because they are paid to sell that advice.

The internal controls related to financial reporting and audit functions, Swensen tells us, are tasks made relatively easy by his emphasis on due diligence and documentation.

There are also questions of oversight, central among which is trustee oversight of the endowment itself. To be a successful active investment manager, Swensen tells us, you must be a contrarian thinker. What kind of oversight is appropriate for a contrarian? How to evaluate the actions of someone who, by definition, is not going to do what you think they will? Oversight should happen on the basis of collegiality first and foremost (304). Swensen sees collegiality as fundamental to the endowment’s whole undertaking both internally (as an organization) and with its various external partners and clients—shared backgrounds, shared milieu, shared basic worldview, same (agency theory) sense of what matters and what does not and of the kind of boundary that separates those things. Alumni of the same school, both within and beyond the endowment.[28] Yale for example:

David Swensen made it fun to work on investing for Yale, recruiting a team of exceptional Yale graduates who, in their first professional jobs get a wide exposure to the world of investing: early responsibility for inquiry, analysis and decisions; and an exemplary exposure to teamwork at work. David Swensen’s “alumni” have gone on to important endowment management posts at the Carnegie and Rockefeller foundations, as well as at Duke and Princeton universities. As Churchill observed: People like winning very much. (Charlie Ellis, Introduction to the 2000 edition, xxi)[29]

In PPM, collegiality permeates formal and informal relationships, extending to a shared interest in poker and willingness to spend Wednesday nights at cards, or interest in and ability at sports, which are strangely important in the finance universe. It is basic to the internal culture of the Yale Model, to how it operates and how it is reproduced across time and/or changes in personnel.

Oversight requires a shared understanding of the rationale that informs a contrarian approach to investment management. And everything is facilitated by the returns, those stellar, lovely returns. Charlie Ellis, who chaired Yale’s endowment committee for much of Swensen’s tenure as CIO, writes:

One secret of Yale’s success has been David Swensen’s ability to engage the committee in governance—and not in investment management. Contributing factors include: selection of committee members who are experienced, hard-working and personally agreeable; extensive documentation of the due diligence devoted to preparing each investment decision; and full agreement on the evidence and reasoning behind the policy framework within which individual investment decisions will be made. As a result, the whole of the investment committee is always conceptually “on board” with overall policy, before turning to specific investment decisions. This pre-empts ad hoc decision-making by individuals determined to be “helpful.” Of course, good results and careful adherence to agreed and articulated policies help too. But the decisive factor is the great confidence David Swensen has earned by constant fidelity to purpose, rigorous rationality, and open, full review of all investment decisions with staff, investment managers and members of his committee (xx)

On the one hand, Ellis describes an admirable degree of openness (within a certain purview). Everyone involved has the background to understand the investment strategy, is persuaded of its validity, and is let in on individual decisions.

“The Yale Model,” at Yale, where it is not a model, may not be particularly autocratic but, in many of the places that have adopted it, the Yale Model reinforces autocratic tendencies of administrations that may or may not have been already so inclined.

But what relations obtain between this horizontal, collegial space and the institutional and social contexts beyond it? Consider for example student activists looking to get their college or university to divest its holdings in fossil fuels. Any such campaign should be bothered by the opacity of alternative investments, the absence of disclosures as to their portfolio holdings, and want information from the endowment. What kind of response might such student activists expect? Probably indifference or hostility. One can see a potential explanation in the very fact that the people Ellis refers to believe in Yale’s higher mission, think they are right about what they are doing, and take those returns as confirmation.[30] Ellis gives another indication, one that echoes a theme that has run through this article: the resistance to “ad hoc decision-making” in response to “individuals determined to be ‘helpful.” Being-reactive runs counter to the long-term perspective, which Swensen seems to see as its opposite. Occupying a perspective symmetrical the time-horizon of centuries is doing as the numbers tell you - not reacting, not falling back into patterns familiar from the loser’s game. A third might follow from notions of secrecy and trust among people inside the endowment’s various networks. In 2018, The Detroit Free Press investigated The University of Michigan’s endowment because it had information that the endowment was invested in private funds run by alumni who, in turn, made donations (kickbacks) to the endowment. The paper was not able to penetrate very deeply. Chief Investment Officer L. Erik Lundberg said in an interview: “No-one gives away their secrets.” Despite that the Free Press article is good and well worth your attention. All of these are reinforced by a shared cognitive geography that is encapsulated by agency theory, how it distinguishes inside from outside, what matters from what does not, and who has standing from who does not.

A Concluding Remark

We followed David Swensen in Pioneering Portfolio Management in order to tease out the particular weave of insight and blindness that informed the document that is responsible, more than any other, for laying out the Yale Model and selling it to readers. The first part focused on the problems faced by the figure of the active institutional investor in the 1970s and showed both how Swensen transformed that figure. The second part presented the model. In order to do that, we had to introduce alternative investments as if the reader, like an endowment manager thinking of adopting the model, did not really know what they are. We explored the fashioning of Swensen’s “long-term” viewpoint, with its defining characteristic of not-reacting to “turbulence” in either university or market. We then looked at hedge funds and private equity in terms of how Swensen describes them in PPM, so how “he,” the book’s narrator, “sees them.” We described the endowment as a network in much the same way.

What is visible and what is not in PPM: the exceedingly expensive fees charged investors in hedge funds and private equity are only noted when “excessive” enough to constitute a “misalignment” which is to say when Yale was unable to arrive at side-letter arrangements advantageous to itself. But the normal outflows of huge sums is just the price of doing business, and the fact that the flows of these fees is what holds together the endowment as network goes without saying. Swensen prefers private-equity funds that impose operational changes on acquired companies because that differentiates them from traditional corporate M&A. He sees private-equity LBO strategies figure as an option for portfolio diversification. About the massive socio-economic damage visited upon the non-financial economy by these strategies there is nary a word.

End of Part 2

© Pattern Recognition: A Research Collective, 2023

[1] See The Yale Endowment’s “Yale’s Strategy.”

[2] The Financial Times obituary for Swensen, who died from cancer in May, 2021 at 67 years old, intertwines the two dimensions of Swensen and could be read profitably in light of “Borges and I.”

[3] Yale’s 2020 Endowment Report has an overview of the endowment’s organizational structure on p. 9 and a partial list of Swensen’s more prominent students and proteges beginning on p. 14. Yale’s directory of annual reports and press releases is here. See also here..

[4] We return to the theme of an endowment is a network in this essay’s third section.

[5] Swensen and his colleague called their approach “means-variance” as a tribute to James Tobin, Swensen’s mentor, who also wrote equations crucial to its development.

[6] Interest-rate swaps are contracts with investment banks that allow an issuer to exchange variable for fixed interest rates on a bond. The arrangement can be advantageous where interest rates are volatile, or where there is some reason to expect they will rise. The fixed rate amounts to a bet placed on the future. Many colleges, universities, pension funds and municipalities got into significant trouble with these swaps: see the important 2017 report by Dominic Russell, Carrie Sloan and Alan Smuth for the Roosevelt Institute, “The Financialization of Higher Education: What Swaps Cost our Schools and Students.”

[7] It follows that outside critics would be an obvious problem.

[8] See our explainer document on endowments here.

[9] Metrics that attribute 10% weight to endowment size as a proxy for institutional prestige, with a resulting pressure to hoarding.

[10] MorningStar (mutual fund): “Bond Pricing: Agreeing to Disagree p. 2 “Moving at the Speed of Bonds,” January 20, 2021.

[11] This is a sub-theme in Burroughs and Helyar’s 1989 book Barbarians at the Gate: The Fall of RJR Nabisco. The PE fund KKR relied on junk-bond funding of their bid, which required they put up vastly less of their own money than fund relying on investment bankers alone would have had to.

[12] Marc Gunther, “Yale’s $8 Billion Man” in Yale Alumni Magazine, July/August 2005.

[13] Markowitz’s paper is widely available online. Here is some basic bibliographic information. He was awarded a 1990 Nobel Prize in Economics for his work in this area.

[14] Naess, R. D.. 1949. “The Enigma of Investment Management.” Analysts Journal, vol. 5, no. 3: 5–9, quoted in David Chambers, Elory Dimson and Charikleia Kaffe, “Seventy-Five Years of Investing for Future Generations” in Financial Analyst Journal 76:4 (2020) pp. 5-21, available here.

[15] This was at the time quite radical. See further on, the quote from “Yale’s $8 billion man.”

[16] We will look in a bit more detail at modern portfolio theory in due course.

[17] Rutterford and Sotiropoulos, p. 921 (see note 7).

[18] The other texts included in this collection make those trade-offs and costs clear.

[19] PPM, Investment Process, Decision-Making Process, Policy-Target Focus pp. 315-6. See also “Yale in 1987”, pp. 316-7, for Swensen’s account of the endowment’s (early) decision to react to market turbulence and convene on matters of strategy more than once in that year and why it turned out to be not great.

[20] There’s more to it than this of course. See Swensen’s discussion in PPM pp. 131-6. He covers the general process, the psychology of rebalancing, its frequency and the problems posed by illiquid asset classes. Swensen appears to have often found his risk-management strategy side in conflict with the returns-oriented side over the matter how to deal with the difficulties illiquidity created for rebalancing--but projected returns tended to carry the day (138-9).

[21] A quite remarkable article from Institutional Investor in July 2022 full of pension-fund managers complaining about all the scrutiny they’ve fallen under for not knowing about the fees is available here

[22] “David Swensen’s Guide to Sleeping Soundly

[23] Marc Gunther, “Yale’s $8 Billion Man” in Yale Alumni Magazine, July/August 2005.

[24] When he asked in 2009 why he didn’t open his own hedge fund and make vastly more money than the $4.7 million per annum Yale paid, he shrugged and said he had thought about it and decided “It wasn’t for me.”

[25] For a discussion of the fine line that separates legal from illegal insider information, see Sheelah Kolhatkar’s Black Edge: Inside Information, Dirty Money and the Quest to Bring Down the Most Wanted Man on Wall Street (New York: Random House, 2018).

[26] Breaking register, what Swensen leaves out on debt is how PE fund impose that debt on acquired companies, how they that debt to reorganize those companies in order to maximize extraction, the consequences of these reorganizations on working people in the form of job losses and the relation between PE’s predatory uses of debt and acquired companies ending up in bankruptcy. The business model was problematic from its earliest days of the business model, by 2022 they have only gotten worse.

[27] For a sense of the social destruction, see The Private Equity Stakeholders October 2021 virtual symposium “Workers Challenging Private Equity to Create Good Jobs” and, more generally, their most excellent website.

[28] One thing that does not get mentioned is whether Ellis and Swensen’s relationship constituted a conflict of interest. See the 2010 report by Harvard’s Center for Social Philanthropy and Tellus Institute, “Educational Endowments and the Financial Crisis: Social Costs and Systemic Risks in the Shadow Banking Sytem” pp. 4-5 and pp. 40-55.

[29] Charlie Eaton has been has been exploring the importance of alumni networks to the financialization of higher education more broadly. We look forward to the release of his book Bankers in the Ivory Tower.

[30] But these people are also as one in treating the internal rates of return that private equity funds reported as if they are real. For recent (2021) examples, see here, here or here. Not long after these announcements, in November 2021, Charlie Eaton published a WaPo editorial critical of these numbers. The strongest criticisms of IRR as a metric can be found in Eileen Appelbaum and Rosemary Batt have a compelling critique of IRR in their book Private Equity at Work and in the work of Oxford-based PE critic Ludovic Phallipou. In summary, the latter calls IRR a “garbage number” in his book Private Equity Laid Bare. We will return to this important matter in a sequence on the private equity problem.